Key points:

- U.S. law firms reached record profitability in 2025, fueled by demand volatility and aggressive rate growth.

- That prosperity masks growing structural strain as costs rise faster and AI reshapes how legal work is performed.

- Demand is shifting downstream to lower-cost firms and alternative providers as corporate legal budgets tighten.

- Market indicators point to slowing growth - and possible contraction - by mid-2026.

The 2026 State of the U.S. Legal Market report from the Thomson Reuters Institute, produced with Georgetown Law, presents a paradox. U.S. law firms are delivering some of the strongest financial results in modern history - driven by rate growth and demand volatility rather than underlying economic expansion - even as the foundations of the traditional law firm business model show increasing signs of strain.

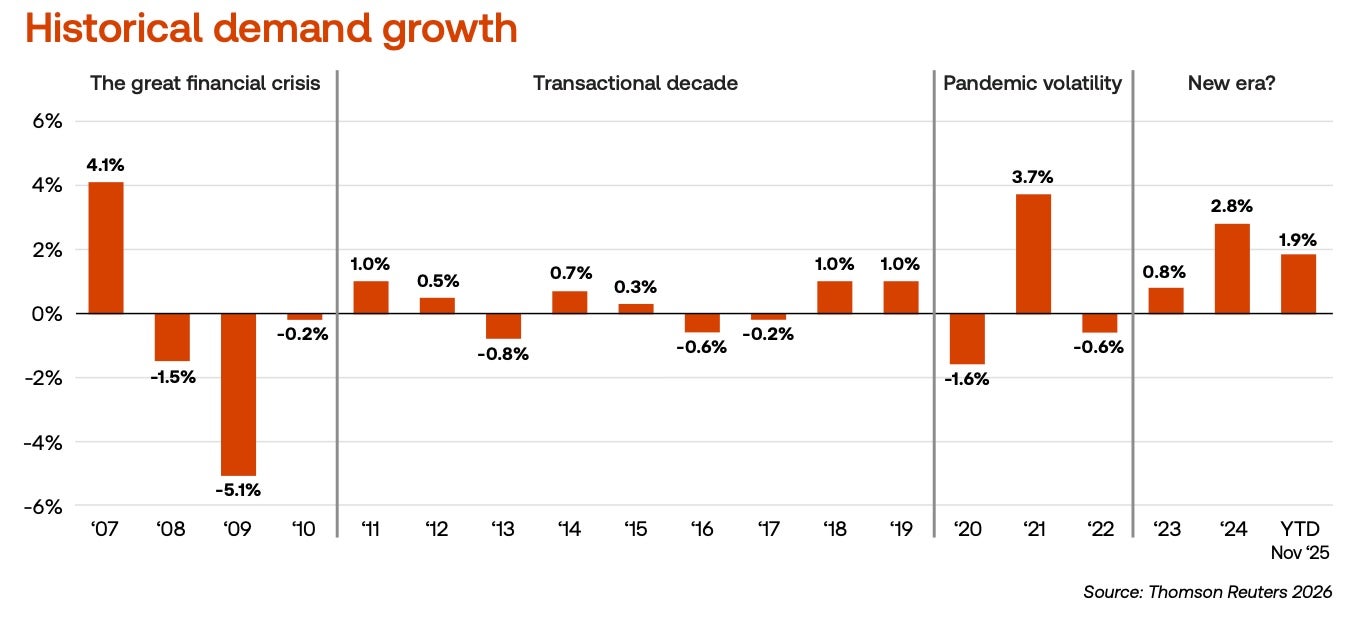

For legal leaders, the report reads less like a victory lap and more like a warning. It characterizes the current moment as one of peak prosperity, driven not by broad economic expansion but by instability - regulatory upheaval, geopolitical risk, and policy volatility that have flooded firms with work. History suggests that when legal demand surges for these reasons, it is often followed by a correction.

Demand is strong - but it is moving.

Legal demand rose nearly 2% in 2025, making it one of the strongest years since the 2008 financial crisis. Much of this demand has been driven not by economic expansion, but by regulatory disruption, geopolitical uncertainty, and policy shifts that increase legal workload without expanding client budgets.

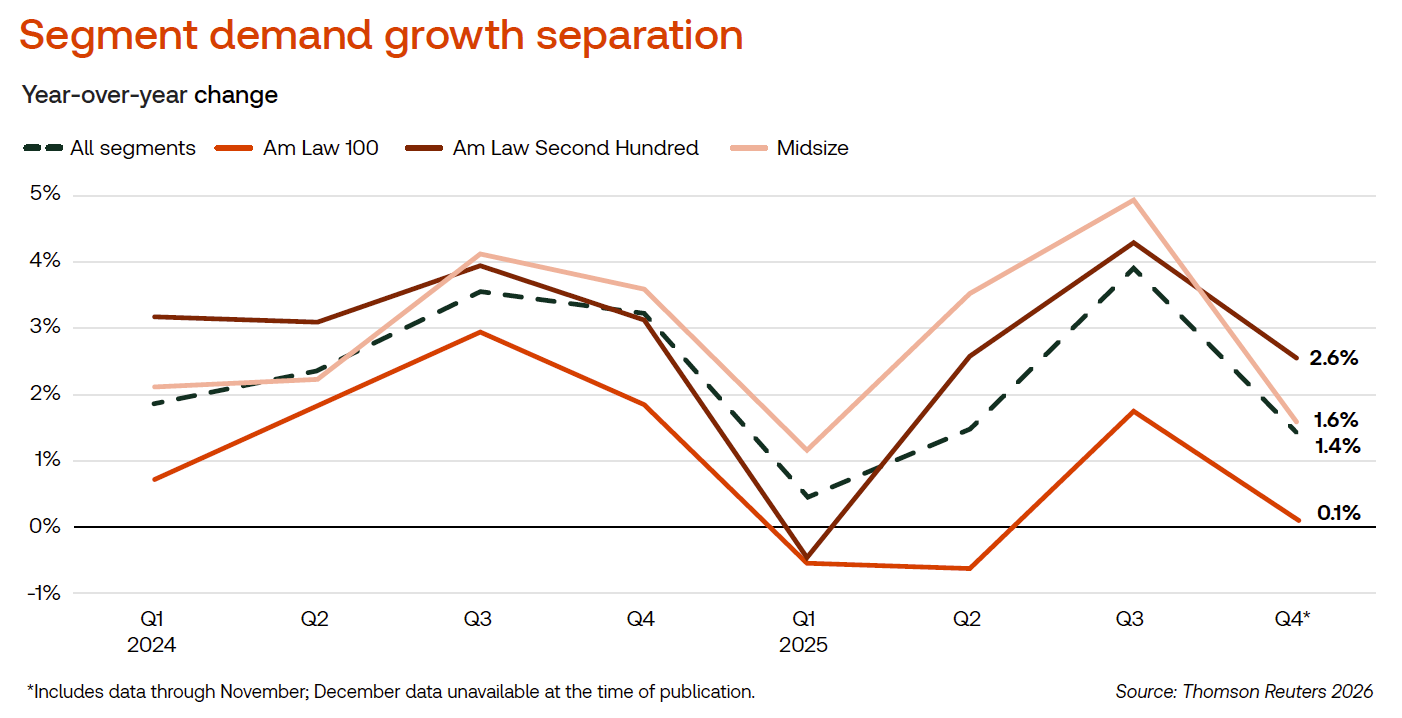

But the growth was uneven. Much of the incremental work flowed away from the most expensive firms toward midsize and lower-cost providers as corporate legal departments rebalanced their portfolios.

Midsize firms captured the largest share of demand growth, while Am Law 100 firms posted materially slower gains and relied on a late-year spike to finish the year in positive territory. The shift reflects deliberate client behavior rather than a temporary pricing dispute.

Facing flat budgets and rising internal expectations, general counsel increasingly pushed routine and moderately complex matters downstream. Clients are becoming more intentional about where premium expertise is required - and where it is not.

Profitability is high, but cost discipline is weakening.

On paper, the industry is thriving. Average law firm profitability increased by roughly 13% in 2025, with profits per lawyer at Am Law 100 firms more than 50% above pre-pandemic levels. These gains were driven by sustained demand and aggressive rate increases, with worked rates rising more than 7% year over year.

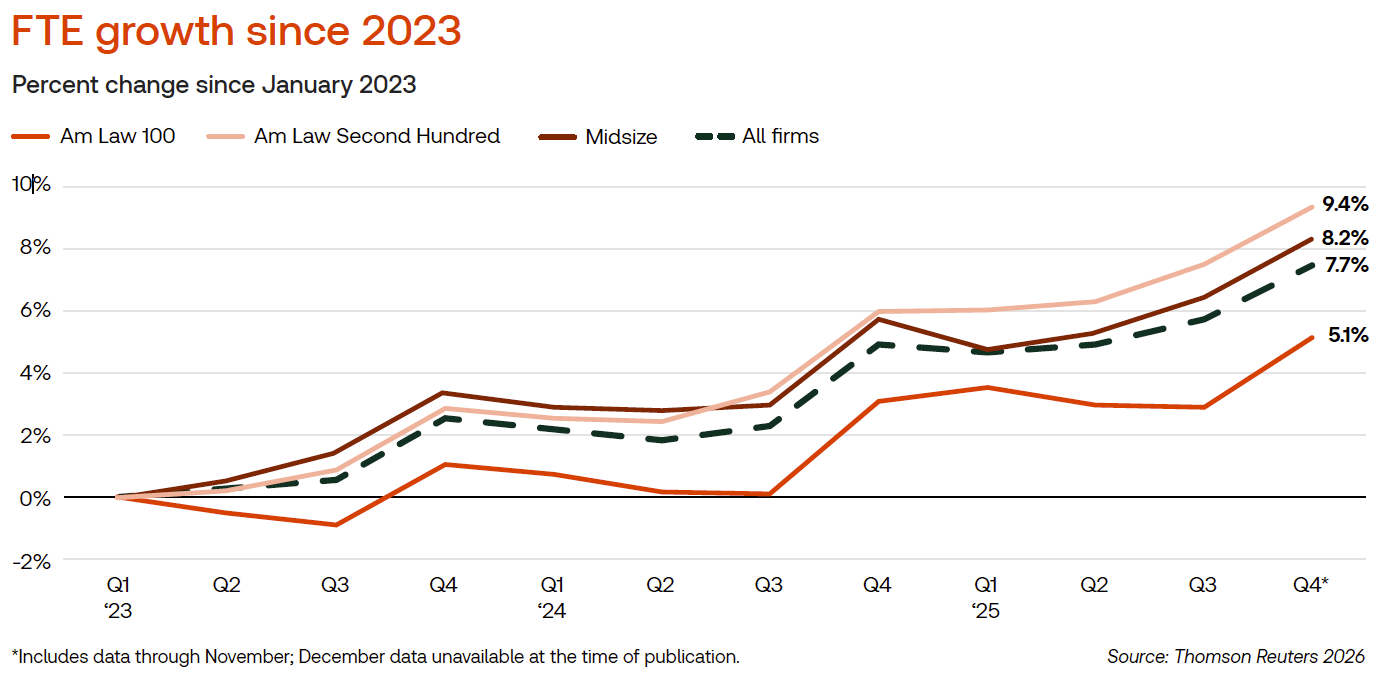

At the same time, firms significantly expanded their cost base. Technology spending rose nearly 10%, driven largely by investments in generative AI and knowledge management tools. Lawyer compensation increased more than 8%, reflecting continued competition for talent and a reluctance to reduce headcount despite efficiency gains.

The result is an industry spending as though current demand conditions will persist. The report cautions that this assumption has proven risky in prior cycles, particularly when rising fixed costs collide with a slowing market.

AI is accelerating a pricing contradiction.

No theme looms larger than the collision between AI-enabled efficiency and the billable hour. Firms are deploying technology that compresses work once measured in hours into minutes - yet nearly 90% of legal revenue is still billed by time.

Many firms have responded by raising rates, arguing that AI enhances the value of legal services rather than diminishing it. Corporate clients, however, remain skeptical. Legal departments increasingly question why productivity gains accrue primarily to outside counsel instead of being reflected in lower costs or alternative pricing structures.

This standoff is becoming harder to sustain. Both sides acknowledge the need for new pricing models, but neither is eager to move first. As AI continues to reduce the time required for routine work, the economic tension underlying hourly billing becomes more exposed.

Alternative delivery is moving from the margins to the mainstream.

Against this backdrop, law firms are expanding their use of alternative legal service providers, flexible staffing models, and hybrid delivery structures. These approaches allow firms to manage costs and preserve margins while responding to client demands for predictability and efficiency.

North American firms still lag peers in Europe and Australia in formal ALSP partnerships, a gap the report identifies as both a risk and an opportunity. As clients increasingly expect integrated solutions that combine automation, lower-cost labor, and legal judgment, firms that resist these models may find themselves structurally disadvantaged.

Client sentiment is turning.

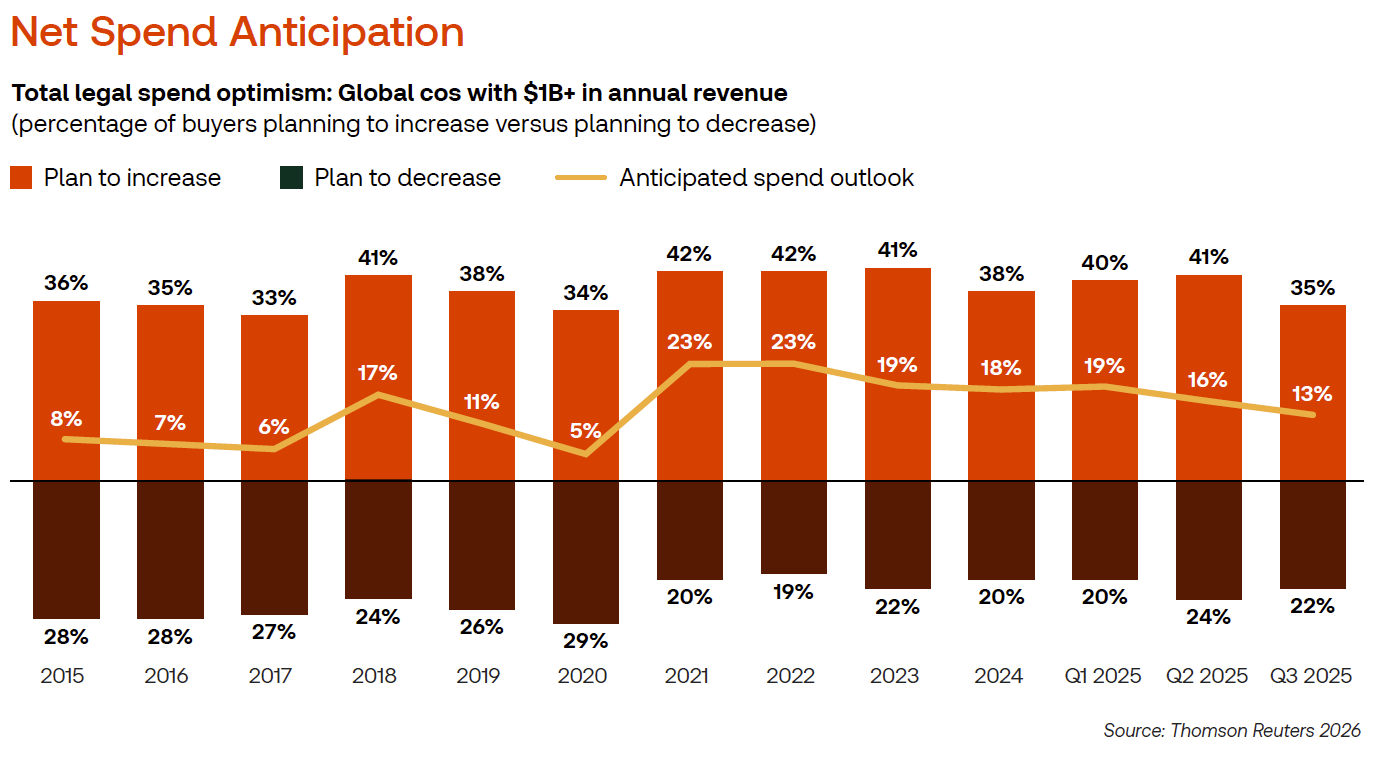

Perhaps the most consequential signal in the report comes from buyer sentiment. Surveys of corporate legal leaders show net spending expectations falling toward pandemic-era lows. Transactional practices that fueled recent profit growth are now among the weakest areas of anticipated demand.

Market forecasts cited in the report point to slowing growth - and the possibility of contraction - by mid-2026. If that scenario materializes, firms carrying higher fixed costs and inflexible pricing models will feel the impact first.

The bottom line.

The legal market is not in crisis, but it is at an inflection point. The forces driving today’s profitability are the same forces destabilizing long-standing assumptions about pricing, leverage, and value.

But the growth was uneven. Much of the incremental work flowed away from the most expensive firms toward midsize and lower-cost providers as corporate legal departments rebalanced their portfolios.

After the report: What in-house teams can do next

As demand shifts and budgets tighten, in-house teams are placing greater emphasis on visibility and market context when making decisions about talent and outside counsel.

- Identify: lower-cost counsel and flexible talent across jurisdictions and roles.

- Benchmark: rates, compensation, and spend against current market data.

- Allocate: work deliberately across firms, regions, and staffing models.

Explore spend management tools for in-house teams | Hire flexible legal talent | Create a free company account